Variable Pay: What It Is and How to Design It

Variable pay is any compensation tied to performance rather than fixed by contract. Here's how to design a program that actually motivates — and what most companies get wrong.

Variable pay is the portion of compensation that changes based on what you do. Base salary is fixed — you earn it for showing up and doing your job. Variable pay is conditional. You earn it by hitting a number, completing a goal, or outperforming a threshold.

For sales roles, variable pay is usually the largest part of total compensation. For most non-sales roles, it's either a small annual bonus or nonexistent. Knowing how to design it — and what separates plans that motivate from plans that frustrate — matters whether you're building a comp program from scratch or evaluating an offer with variable pay attached.

What variable pay is

Variable pay is any compensation that isn't fixed by contract and changes based on individual, team, or company performance. The fixed component is base salary. Everything tied to outcomes is variable.

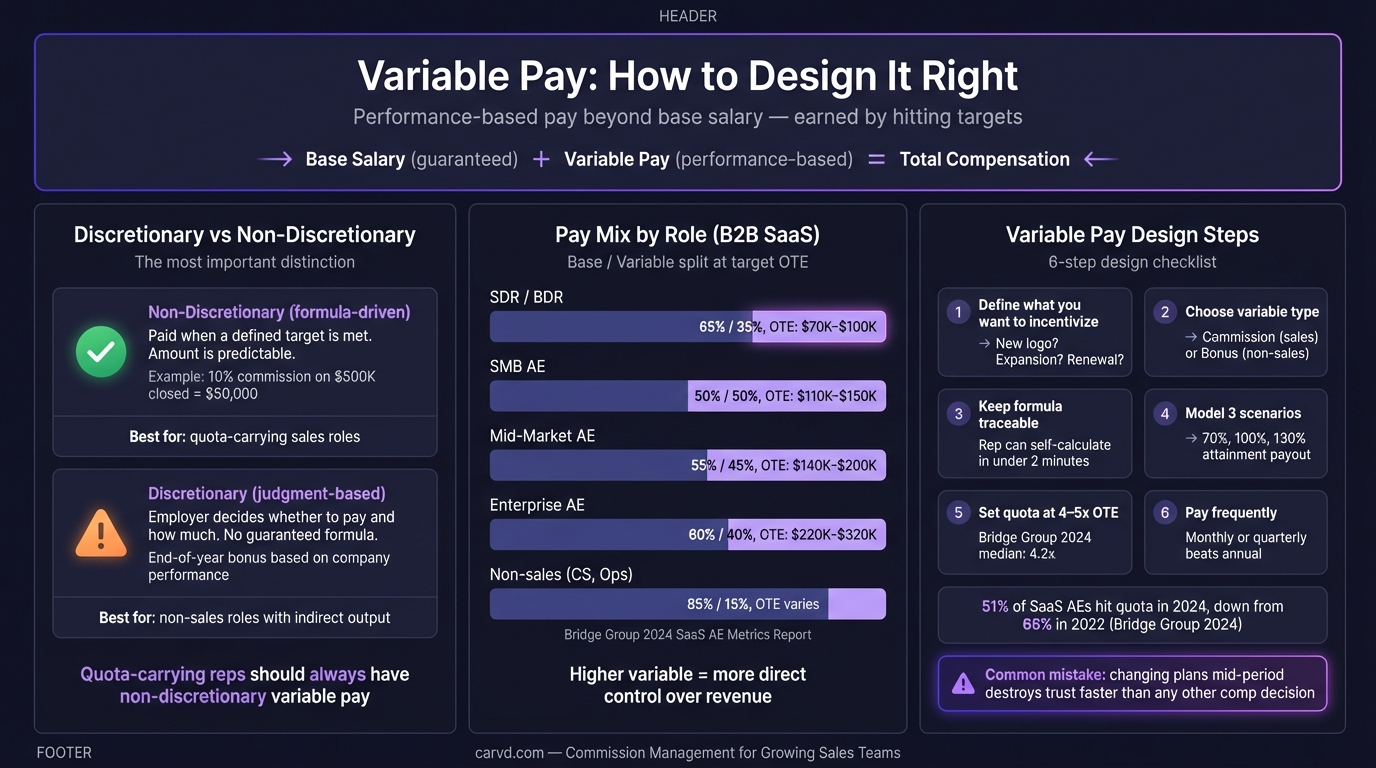

The ratio of base to variable is called pay mix. A 50/50 pay mix means half your total compensation is base, half is variable. A 70/30 mix means the job leans more stable, with less upside.

Variable pay comes in several forms:

- Commission — a percentage of revenue tied to individual sales output, typically per deal closed

- Bonuses — lump-sum payments for hitting a defined goal, often quarterly or annual

- SPIFFs — short-term cash incentives for specific products or behaviors in a defined window

- Profit sharing — a share of company profits distributed to employees, usually annually

- Accelerators — commission multipliers that kick in above quota, rewarding overperformance

For a full breakdown of each type and how they work in sales comp plans, see variable compensation: types, structures, and best practices.

Variable pay vs fixed pay

The choice between variable and fixed pay isn't philosophical — it's practical. It depends on how directly a role connects to a measurable revenue outcome.

When variable pay makes sense:

- The role directly closes, generates, or expands revenue

- Individual output is measurable (deals closed, pipeline created, accounts retained)

- Performance varies meaningfully across the team (some people close 3x what others do)

- You want to reward top performers more than average performers

When fixed pay makes sense:

- The revenue connection is indirect or long-delayed

- Individual output is hard to isolate from team or product factors

- Consistency and reliability matter more than upside

- The role requires long time horizons where variable pay creates short-term bias

Most sales organizations design variable pay for closing AEs, SDRs, and account managers. They keep other roles on fixed pay or add a modest annual bonus. That's a reasonable default. The mistake is applying variable pay to roles where the line-of-sight between behavior and payout is too fuzzy to motivate — you get the administrative overhead of a variable pay program without the motivational benefit.

How to design a variable pay program

Step 1: Define eligibility clearly

Not everyone needs variable pay. Start by identifying which roles have direct, measurable impact on revenue. Closing AEs are the clear case. SDRs and account managers usually qualify. Engineers, operations, and support typically don't — unless you're running a company-wide profit sharing program separate from individual variable pay.

Write down who's eligible, what they're eligible for, and when payouts occur. Ambiguity in eligibility is the first thing that creates disputes.

Step 2: Set OTE from market benchmarks, not internal math

OTE (on-target earnings) is the total a rep earns when hitting 100% of quota — base plus variable at target. It should start with what the market pays for the role, not with what you can afford.

For sales roles, the right sources are the Bridge Group's annual SaaS benchmarks, Betts Recruiting compensation reports, and RevOps community surveys like Pavilion. For non-sales variable pay (annual bonuses, profit sharing), WorldatWork publishes broad compensation benchmarks across industries.

If OTE is set below market, top candidates will negotiate it up or take an offer elsewhere. If it's set significantly above market, you're overpaying and will struggle to scale the comp program as the team grows.

Step 3: Choose the right pay structure for the role

Pay structure determines how variable pay accrues and when it pays out.

| Role | Typical structure | Payout cadence |

|---|---|---|

| Closing AE | Commission (% of ACV) | Monthly or quarterly |

| SDR/BDR | Bonus on pipeline/meetings | Monthly or quarterly |

| Sales manager | Team quota attainment bonus | Quarterly |

| Account manager | Retention + expansion commission | Monthly or quarterly |

| Non-sales employee | Annual performance bonus | Annual |

Commission pays out per deal — it's real-time reinforcement of the behavior you want. Use the commission plan builder to model how different structures affect payout at various attainment levels. Annual bonuses are less effective at changing day-to-day behavior because the payout is too far away. For sales roles, shorter-cycle payout cadences are almost always better.

Step 4: Set targets that are achievable by most of the team

A variable pay program where fewer than half the team earns at target isn't a pay program — it's an aspiration. If you're consistently seeing 30% of the team hit quota, the quota is wrong, not the reps.

A common design principle: 60–70% of eligible employees should earn at or above their variable target in a normal year. That's not lowering the bar — it's validating that the target is calibrated to what's actually achievable with reasonable effort.

Step 5: Add accelerators for overperformance

Variable pay that caps out at 100% quota attainment leaves money on the table for top performers — and drives them toward employers who offer more upside. Accelerators (higher commission rates or bonus multipliers above quota) are the primary retention tool for the top quartile of any sales team.

A standard accelerator structure: 1.0x rate up to 100% quota, 1.5x between 100–120%, 2.0x above 120%. The exact thresholds depend on your margins and what you're willing to pay, but the principle is consistent: make overperformance materially worth staying for.

Step 6: Communicate the plan before the period starts

Variable pay only motivates behavior it can influence. If a rep learns their Q1 commission rate in March, it didn't affect anything they did in January and February.

Plan communication should happen before the period begins. That means: written plan documents, a walkthrough explaining how payouts are calculated, and a way for reps to see their running payout throughout the period — not just at the end of it.

Transparency is a design requirement, not a nice-to-have. Carvd's rep dashboards give each rep real-time visibility into quota attainment and projected payouts, so they can verify their own number without asking ops. If reps can't calculate their own payout within a few minutes of closing a deal, the plan will generate shadow accounting — reps independently tracking their own numbers in parallel because they don't trust what finance reports. That's a waste of selling time and a reliable signal of a comp plan problem.

How variable pay is taxed

This matters for both employees evaluating offers and employers managing payroll.

The IRS treats commissions, bonuses, and other variable pay as supplemental wages. The flat federal withholding rate for supplemental wages is 22% on amounts up to $1 million per calendar year (37% above $1 million). States apply their own withholding on top.

One important nuance: the 22% withholding rate is not the final tax rate. At year-end, all income — base salary and variable pay — is combined and taxed at the employee's effective rate. If that rate is higher than 22%, the difference is owed. If lower, it results in a refund.

Employees sometimes feel variable pay is "taxed more" because a large commission check has a flat 22% withheld upfront. It's not taxed differently — it's withheld differently. The total tax at year-end is the same either way.

For employers: commissions and bonuses are fully deductible as ordinary business expenses. However, under ASC 606, commissions paid to acquire customer contracts may need to be capitalized and amortized over the expected customer lifetime rather than expensed immediately. See commission accounting under ASC 606 for more.

Common variable pay design mistakes

Setting commission rates before quota math

The commission rate should be derived from OTE and quota — not chosen independently. If OTE is $180,000 with a 50/50 split, the variable target is $90,000. If quota is $1M, the commission rate is 9%. Many companies pick a rate like "10%" and then try to fit quota around it, which often results in quotas that don't match market expectations.

Variable pay without a calculation method reps can verify

If reps can't check their own payout in real time, the variable pay program creates anxiety instead of motivation. Every plan should have a written formula, examples showing how it applies to real deals, and ideally a live dashboard. Tools like Carvd calculate deal-by-deal commission breakdowns so reps can see exactly how their variable pay was derived — which eliminates the shadow accounting problem.

Changing the plan mid-period

Adjusting targets or rates during an active period destroys trust faster than almost any other comp mistake. Even if the adjustment is well-intentioned (market conditions changed, initial quota was wrong), it signals that the plan isn't stable. Reps stop relying on the plan to forecast their income and start hedging.

Over-complexity

Every additional condition, qualifier, or exception in a variable pay plan adds administrative overhead and reduces clarity. The best plans have one or two payout levers — quota attainment and accelerators. Plans with five interdependent variables create calculation disputes and drain sales ops time. When disputes do arise, a structured dispute resolution process keeps them from escalating into trust problems.

When variable pay doesn't work

Variable pay underperforms when:

- Targets are unachievable — if fewer than 40% of the team consistently earns at target, trust in the plan collapses and it stops driving behavior

- Payout cycles are too long — annual bonuses rarely change what people do in January

- The formula is opaque — reps who can't self-calculate their commission develop shadow accounting and distrust

- Quotas aren't validated — territory coverage, deal volume, and average deal size need to support the quota before it goes live

None of these are failures of variable pay as a concept. They're failures of design and execution.

Related reading: Variable Compensation: Types, Structures, and Best Practices · On-Target Earnings: The Complete Guide · Sales Compensation Plan: How to Build One · OTE vs Base Salary

Last updated: March 22, 2026