Sales Commission Tax: Withholding, Reporting & State Rules

How to handle commission withholding, W-2 vs 1099-NEC reporting, state tax rules, and year-end reconciliation for sales teams paying commissions.

Paying commissions involves two separate tax obligations: withholding correctly when you pay and reporting accurately at year-end. Both carry penalties if handled incorrectly. The mechanics depend on whether the payee is a W-2 employee or a 1099 contractor — and which state (or states) they work in.

This covers the employer and finance team perspective. If you're a rep trying to understand what will come out of your check, see commission tax rate and is commission taxed differently. For the full picture on commission taxation, see how are commissions taxed.

How commissions are classified

The IRS classifies commission payments to W-2 employees as supplemental wages — compensation paid in addition to, or separately from, regular pay. Per IRS Publication 15, supplemental wages include commissions, bonuses, overtime pay, and severance. This classification determines which withholding method applies.

Commissions paid to independent contractors fall outside the supplemental wage rules entirely. There's no withholding obligation — the contractor receives gross payment and handles their own tax obligations.

Withholding on employee commissions

For W-2 employees, you have two withholding options when paying commissions. The choice is yours as the employer.

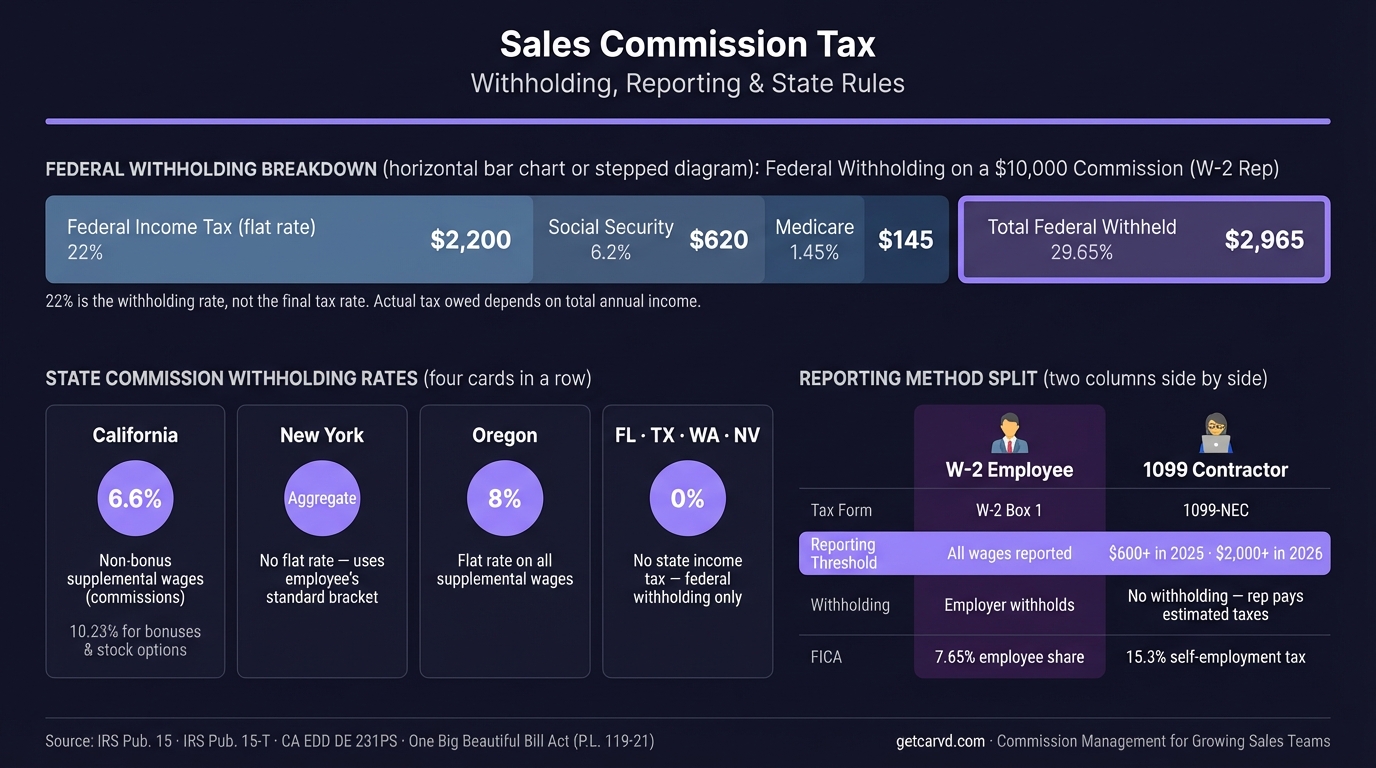

Option 1: Flat 22% supplemental rate

If you pay commissions on a separate check (not combined with regular wages in the same payment), you can withhold federal income tax at the flat 22% supplemental rate. This is the most common approach because it's straightforward: multiply the commission by 22%, withhold that amount for federal income tax, then add FICA.

A $15,000 commission check using the flat rate:

| Component | Amount |

|---|---|

| Commission | $15,000 |

| Federal income tax (22%) | $3,300 |

| Social Security (6.2%) | $930 |

| Medicare (1.45%) | $217.50 |

| Total withheld | $4,447.50 |

| Net to employee | $10,552.50 |

For commissions that push an employee's total supplemental wages above $1 million in a calendar year, the excess must be withheld at 37% — mandatory, not optional — per IRS Publication 15.

Option 2: Aggregate method

You can also combine the commission with the employee's regular wages in a single payment and apply standard withholding tables based on the W-4 on file. Or, if you pay separately, you can calculate what the combined paycheck would have been and withhold the incremental tax.

The aggregate method can result in more accurate withholding for employees whose marginal rate differs significantly from 22%. It's more complex to calculate, which is why most payroll processors default to the flat rate.

FICA withholding — Social Security at 6.2% (up to the $184,500 wage base for 2026) and Medicare at 1.45% — applies the same way regardless of which income tax withholding method you use.

W-2 reporting for employee commissions

At year-end, employee commissions are reported in Box 1 of Form W-2 — the same box that contains salary, bonuses, and tips. There is no separate W-2 box for commissions. This is by design: the IRS taxes commissions as ordinary wage income, identical to salary.

The amounts withheld appear in:

- Box 2: Federal income tax withheld (includes the 22% withheld on commission checks)

- Box 4: Social Security tax withheld

- Box 6: Medicare tax withheld

- Box 16/17: State wages and state income tax withheld (if applicable)

One implication for reps: they won't see commissions broken out separately on their W-2. If a rep disputes the total, the breakdown needs to come from pay stubs or your commission tracking system — not from the W-2 itself. This is one reason why having accurate commission records matters; disputes about year-to-date comp are easier to resolve when you can pull deal-level data, not just payroll summaries. Giving reps access to a rep dashboard with deal-by-deal breakdowns eliminates most of these year-end discrepancies before they escalate.

1099-NEC reporting for contractor commissions

If you pay commissions to independent contractors (1099 workers), the reporting rules are different:

No withholding required. You pay the gross commission. The contractor is responsible for income tax and self-employment tax (15.3% on net earnings).

Form 1099-NEC filing is required when you pay $600 or more to a single contractor in a calendar year. Report the total in Box 1 (Nonemployee Compensation). The $600 threshold applies through 2025; for payments made after December 31, 2025, the threshold rises to $2,000 per the IRS's updated rules.

Deadlines:

- Recipient copy (to the contractor): January 31

- IRS filing: January 31 (electronic or paper)

Penalties for late filing range from $60 per form (if filed within 30 days of the deadline) to $310 per form (if filed after August 1) to $660 per form for intentional disregard, per IRS Publication 1220. If you have multiple contractors, the penalties add up.

Backup withholding: If a contractor fails to provide a valid TIN (taxpayer identification number) or the IRS notifies you of a mismatch, you must withhold 24% of each payment. Collect Form W-9 before issuing the first payment — not at year-end — to avoid this situation.

State withholding on commissions

Every state that has income tax has its own rules for supplemental wage withholding. Most don't follow the federal 22% flat rate.

| State | Supplemental withholding rate |

|---|---|

| California | 6.6% (optional flat method) |

| New York | 11.7% |

| Oregon | 8% |

| Colorado | 4.25% |

| Illinois | 4.95% |

| Texas, Florida, Nevada, WA | No state income tax |

The full list runs to 40+ states with varying rates, thresholds, and methods. Check each state's withholding publication or use a payroll provider that handles state supplemental rates automatically.

Where it gets complicated: multi-state reps. If a sales rep lives in New Jersey but closes deals primarily in New York, you may have withholding obligations in both states. The rules vary by state — some tax income earned in the state regardless of where the employee lives; others follow the employee's home state. Multi-state commission payroll is a compliance area where getting it wrong creates back-withholding issues for both the employer and the rep.

For remote sales teams with reps spread across multiple states, payroll software that handles nexus and multi-state withholding automatically is worth the cost. The payroll export in Carvd gives your payroll provider the finalized per-rep commission totals they need to apply the correct state withholding rates.

Year-end reconciliation

Before issuing W-2s and 1099-NECs, reconcile your commission records against payroll:

-

Match commission totals per rep against what's recorded in your payroll system. Timing differences (commissions earned in December but paid in January) need to be tracked — the W-2 reflects what was paid in the calendar year, not what was earned.

-

Verify FICA wage bases. For employees who earned over $184,500 in total W-2 wages during 2026, Social Security withholding should have stopped once they crossed the wage base mid-year. Check that no Social Security was over-withheld on late-year commissions.

-

Reconcile 1099-NEC totals. Total the commission payments to each contractor from your AP records and match against what's been recorded for 1099 filing. Missing a contractor or underreporting commission income is a common audit trigger.

-

Pull dispute and adjustment records. If a commission was paid in Month 3 and clawed back in Month 7 for a churned deal, how was the clawback handled — was it a repayment or a deduction from a future check? Each treatment has different tax implications. Repayments of previously taxed wages may require a W-2c if the amounts are material. Tracking these adjustments in a commission spreadsheet template or dedicated software keeps the audit trail clean for year-end reconciliation.

Commission tracking software like Carvd generates deal-level commission records throughout the year, which makes year-end reconciliation substantially faster than reconstructing commission history from spreadsheets or email.

Common compliance mistakes

Misclassifying employees as contractors. Paying someone as a 1099 to avoid employer FICA and withholding obligations doesn't hold up if the IRS's behavioral and financial control tests indicate an employment relationship. Misclassification carries back-payroll-tax liability plus penalties.

Failing to file 1099-NECs on time. The January 31 deadline is firm. Many businesses treat it as an afterthought and collect W-9s in mid-January, which doesn't leave enough time to handle errors in TINs or addresses. Set a December deadline internally for all contractor W-9 collection.

Not accounting for state obligations. A common gap: businesses withhold and remit federal taxes correctly, then overlook state withholding registration in states where remote reps have created nexus.

Ignoring backup withholding notices. If the IRS sends a "B notice" (CP2100 or CP2100A) indicating a TIN mismatch, you have 15 business days to act. Missing the backup withholding start date creates liability for the amount that should have been withheld.

Related resources

- Commission tax rate — the 22% withholding rate explained for reps

- Is commission taxed differently — why withholding and actual tax differ

- 1099 commission — tax treatment for contractor commission income

- Commission accounting — how commissions are recorded under GAAP and ASC 606

Last updated: March 22, 2026