Commission Tax Rate: What Sales Reps Actually Pay

Commission withholding runs at 22% flat — but that's not your actual tax rate. Here's how commissions are taxed for W-2 reps and 1099 contractors.

The 22% number on a commission check is not your tax rate. It's a withholding rate — a payroll shortcut the IRS allows employers to use when paying commissions on a separate check. Your actual tax rate depends on your total annual income, deductions, and filing status, the same as for any other earned income.

That gap between withholding and actual tax is why some reps get meaningful refunds in April and others get hit with a bill. Understanding how commissions are taxed — and how withholding works — helps you plan instead of guess.

For a broader overview of how commissions interact with federal taxes, see how are commissions taxed.

The 22% withholding rate explained

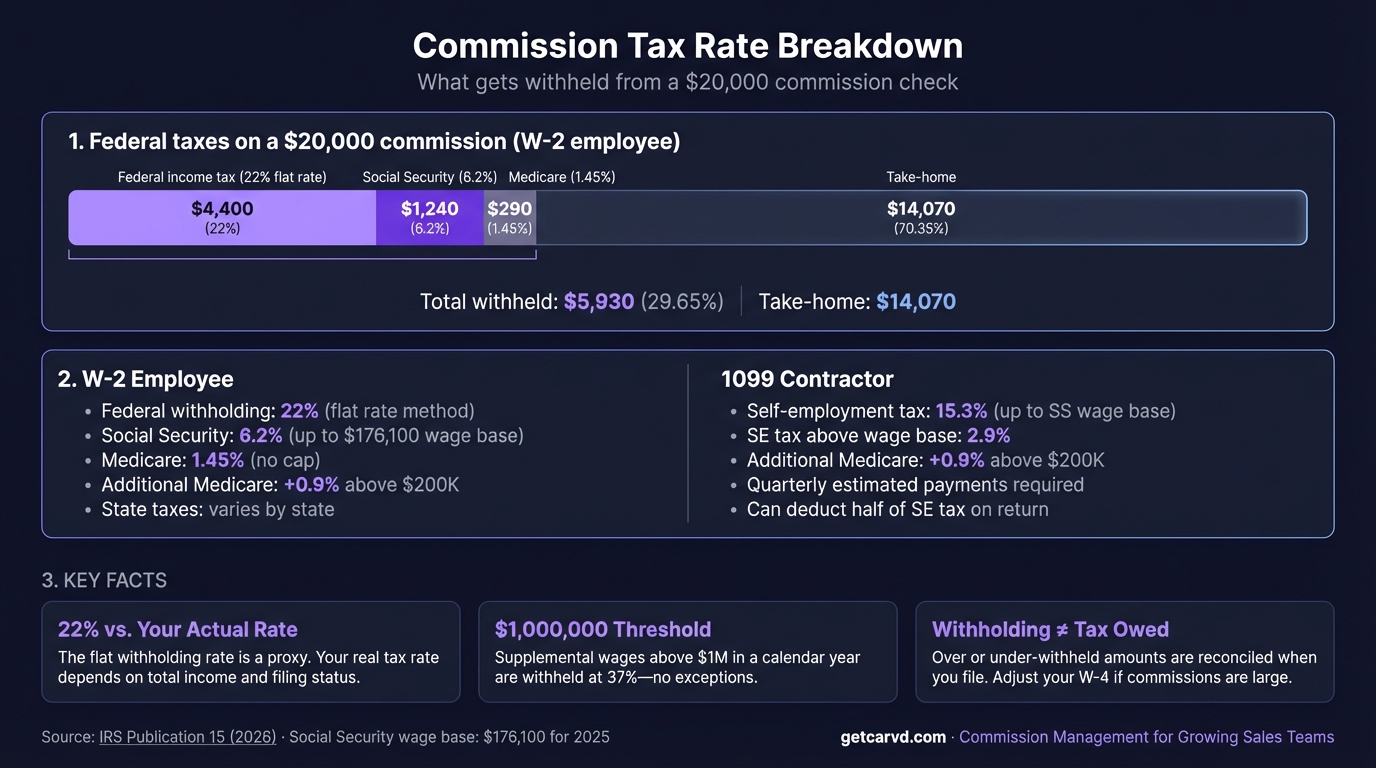

Under IRS Publication 15-T (2026), when an employer pays commissions on a separate check from regular wages, they may withhold federal income tax at a flat 22% supplemental rate. This is optional — the employer can also use the aggregate method — but the flat rate is the most common approach because it's simpler.

The 22% applies to commissions up to $1 million in a calendar year. For any commissions beyond $1 million, the mandatory withholding rate jumps to 37%. Most reps aren't in that territory, but it matters for high-performing enterprise reps with large annual payouts.

Both rates were established by the Tax Cuts and Jobs Act of 2017, which lowered the supplemental rate from the prior 25%. IRS Publication 15-T confirms both are unchanged for 2026.

What this means in practice: A $20,000 commission check will have $4,400 withheld for federal income tax (22%) before FICA. If your actual federal marginal rate is lower — say you're in the 22% bracket but your effective rate across all income is closer to 17% — you'll get the difference back when you file.

The reverse is also true. If you're in the 32% or 35% bracket, the 22% flat withholding on commissions is below your marginal rate, and you'll owe additional tax at filing. This catches some high-earning reps off guard in Q1. Running your expected deals through a commission calculator before year-end helps you estimate total variable income and plan withholding accordingly.

FICA taxes on commissions

Beyond income tax, W-2 commission income is subject to FICA withholding at the same rates as regular wages:

| Tax | Employee share | Employer share |

|---|---|---|

| Social Security | 6.2% | 6.2% |

| Medicare | 1.45% | 1.45% |

| Total FICA | 7.65% | 7.65% |

The Social Security portion applies only up to the wage base — $184,500 for 2026 (up from $176,100 in 2025, per the Social Security Administration). Once you've earned $184,500 in W-2 wages in the calendar year, no further Social Security withholding applies to commissions or salary.

Medicare has no cap. The 1.45% applies to every dollar you earn.

There's also an Additional Medicare Tax of 0.9% on wages above $200,000 for single filers ($250,000 married filing jointly), per IRS Topic 751. This is employee-only — no employer match — and applies at the W-2 level. High-earning reps who hit this threshold will see the extra 0.9% on their commission checks once their year-to-date wages cross $200,000.

W-2 vs. 1099: the FICA difference

For W-2 employees, the employer picks up half of FICA — 7.65% of your wages. You pay the other 7.65%.

For 1099 contractors receiving commission payments, the economics are different. There's no employer picking up the other half. You pay both sides as self-employment (SE) tax:

- 15.3% SE tax on net self-employment income (12.4% Social Security + 2.9% Medicare)

- Social Security applies to the first $184,500 of net SE income for 2026

- The Additional Medicare Tax of 0.9% applies above $200,000 in net SE income

The one offset available to 1099 contractors: you can deduct half your SE tax from gross income on Schedule 1 of Form 1040. This partially replicates the employer-paid share that W-2 employees get but never see.

Quarterly estimated payments: If you expect to owe $1,000 or more in federal taxes for the year, you're required to make quarterly estimated payments using IRS Form 1040-ES. The due dates are April 15, June 15, September 15, and January 15. Missing these results in underpayment penalties — which compound interest regardless of whether you pay the full balance by April.

Most tax advisors suggest 1099 commission contractors set aside 25–30% of gross commission income to cover federal income tax plus SE tax. The right percentage depends on your total income, deductions, and filing status — but 25% is a reasonable starting floor. Keeping a deal-by-deal record in a commission spreadsheet template makes quarterly estimated payment calculations significantly easier.

Why commissions feel taxed more than salary

They're not — but the perception is real, and it comes from how payroll handles separate commission checks.

When your employer runs your $5,000 monthly salary through payroll, the withholding algorithm (based on your W-4) might calculate $650 in federal income tax, producing an effective in-period rate around 13%.

When your employer cuts a separate $20,000 commission check, they apply 22% flat: $4,400 withheld. That looks dramatically higher than your salary check rate, which triggers the perception that commissions are penalized.

What's actually happening: the salary withholding uses a relatively low marginal rate because your W-4 is calibrated to your base salary. The commission withholding uses a flat rate that happens to be higher than many reps' effective rate. At the end of the year, the IRS doesn't care whether income came from salary or commissions — it all pools together and is taxed at the same brackets.

The aggregate withholding method (where commission and salary are combined on one check) often produces even higher single-period withholding, because the combined total inflates that payroll period's annualized income estimate. Same income, higher in-period withholding, same year-end taxes.

State income tax on commissions

Most states that collect income tax apply a supplemental withholding rate to commissions paid on separate checks. A few of the common rates for 2026:

| State | Supplemental withholding rate |

|---|---|

| California | 6.6% (most commissions) |

| New York | 11.7% |

| Oregon | 8.0% |

| Minnesota | 6.25% |

| Virginia | 5.75% |

Nine states have no state income tax at all: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

For reps working remotely across state lines, the rules get more complex. Withholding is typically based on the state where work is performed, not where the rep lives — which can mean multi-state withholding for reps who split time across offices or work in a different state than their employer. If you're in that situation, IRS Publication 15-A and your state's department of revenue have the authoritative guidance.

What this means for commission planning

For reps: the 22% federal withholding on commission checks is often not your actual marginal rate. If you're in the 22% bracket, withholding matches your marginal rate and you'll roughly break even. If you're below that bracket, expect a refund. If you're above it, budget for a tax payment.

If you're getting large commission payouts and not sure whether your withholding is tracking your actual liability, IRS Publication 505 (Tax Withholding and Estimated Tax) walks through how to check. You can also adjust your W-4 to increase withholding on your salary checks to compensate for under-withholding on commissions.

For finance teams calculating the cost of a commission plan: the employer's all-in cost includes the commission amount plus 7.65% in matching FICA (up to the wage base for Social Security), plus any state unemployment and payroll taxes. A $10,000 commission costs the employer roughly $10,765 in direct payroll costs before any other overhead. The payroll export feature in Carvd sends finalized commission amounts directly to your payroll system, so withholding is applied to accurate numbers from the start.

Tools like Carvd calculate commission payouts at the deal level, which gives payroll the numbers they need to run accurate withholding and gives finance a clean record for accounting.

Quick reference: commission tax rates for 2026

| Item | Rate |

|---|---|

| Federal supplemental withholding (under $1M/year) | 22% |

| Federal supplemental withholding (over $1M/year) | 37% mandatory |

| Social Security withholding (W-2, employee) | 6.2% (cap: $184,500) |

| Medicare withholding (W-2, employee) | 1.45% (no cap) |

| Additional Medicare Tax | 0.9% over $200K |

| Self-employment tax (1099) | 15.3% |

| Commissions taxed higher than salary? | No — same ordinary income brackets |

For more on commission tax topics, see is commission taxed differently and 1099 commission. For the employer-side accounting treatment of commission expense, see commission accounting.

Last updated: March 22, 2026