How Are Commissions Taxed? A Complete Guide for Sales Teams

Commissions are ordinary income taxed at the same federal brackets as salary. But withholding works differently — here's how commission taxes work for W-2 reps and 1099 contractors.

Commissions are ordinary income. They're taxed at the same federal brackets as your base salary — no penalty rate, no special category. A rep who earns $80,000 in base and $40,000 in commissions has exactly the same federal tax liability as a rep who earns $120,000 in salary with no commission at all.

The confusion is real, though. Commission checks often look like they're getting hit harder than salary checks. That's not a tax rate difference — it's a withholding mechanics issue. Understanding the distinction matters because it determines whether you get a refund in April or owe a bill.

This guide covers how commission income moves through the federal tax system: the withholding methods, FICA, the W-2 vs. 1099 divide, how commissions compare to bonuses, state-level rules, and what both reps and finance teams need to know when planning comp.

The key distinction: withholding vs. actual tax

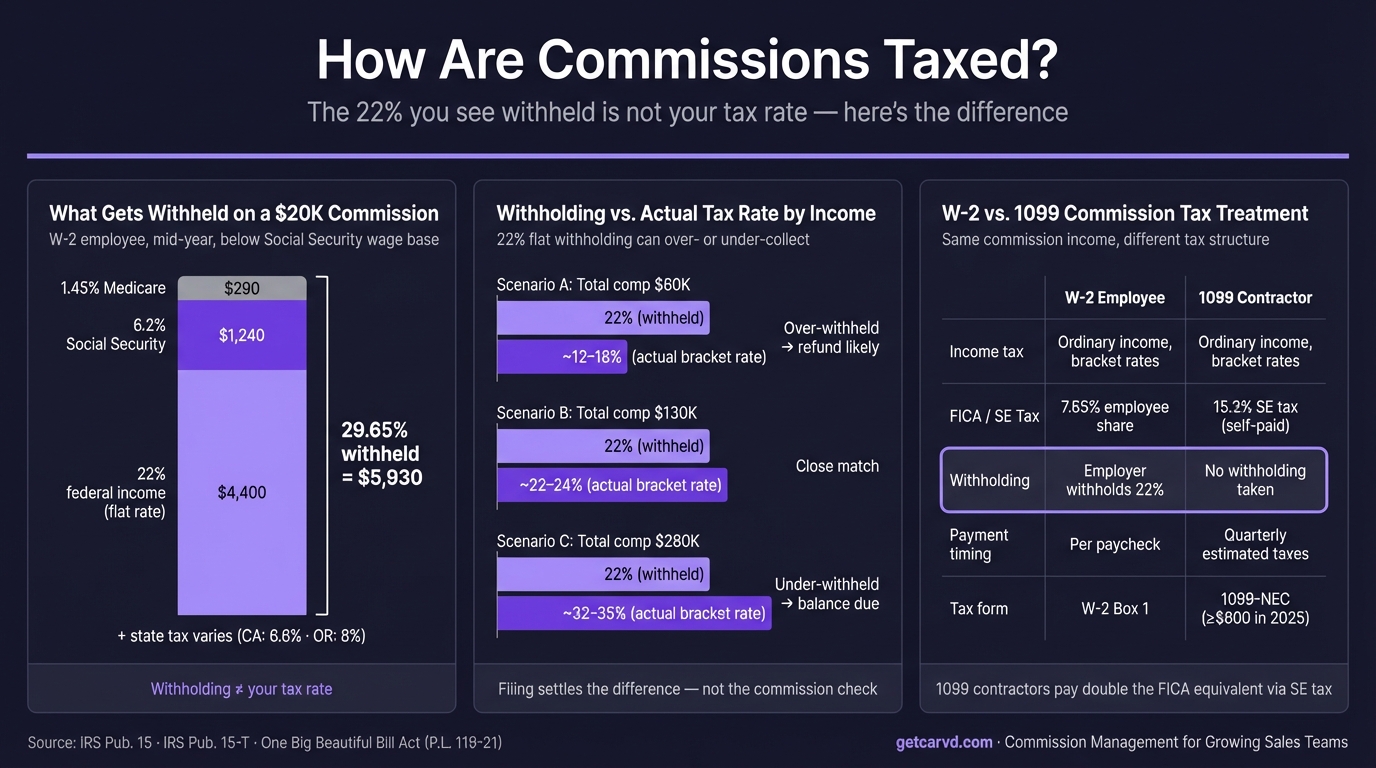

When you see a large deduction on a commission check, you're usually looking at withholding — a prepayment toward your annual tax bill, not your final tax rate.

Withholding is the amount an employer deducts from your paycheck each period and sends to the IRS on your behalf. It's an estimate. The IRS doesn't know your total annual income, deductions, or filing status until you file — so payroll uses formulas to approximate what you'll owe.

Actual tax is determined when you file your return. The IRS applies the federal income tax brackets to your total income for the year, subtracts deductions and credits, and calculates what you owe. Withholding is credited against that liability. If withholding exceeded your actual tax, you get a refund. If it fell short, you owe the difference.

For commission income, this gap is common. The 22% flat withholding on a separate commission check is often higher than a mid-range rep's effective federal rate — producing a refund at filing — and lower than a high earner's marginal rate — producing a tax bill. Neither outcome means commissions were taxed "wrong." It means the prepayment estimate was off.

Federal income tax: ordinary income brackets apply

The IRS classifies commissions as ordinary income under the Internal Revenue Code, the same category as wages, salary, bonuses, and tips. All earned income is pooled on your W-2 in Box 1 — the IRS doesn't see "salary" and "commission" as separate line items with different rates.

Federal income tax brackets for 2026 apply to your total taxable income:

| Taxable income (single) | Federal rate |

|---|---|

| Up to $11,925 | 10% |

| $11,926–$48,475 | 12% |

| $48,476–$103,350 | 22% |

| $103,351–$197,300 | 24% |

| $197,301–$250,525 | 32% |

| $250,526–$626,350 | 35% |

| Over $626,350 | 37% |

These are marginal rates — each bracket applies only to income within that range, not to your total income. A rep who earns $150,000 total (salary + commissions) does not pay 24% on all of it. They pay the lower rates on the first $103,350 and 24% only on the income above that threshold. If you want to model how bracket stacking affects a specific deal, Carvd's commission calculator lets you run scenarios at the deal level.

Because commissions pool with salary to determine total income, a large Q4 commission can push a rep into a higher bracket for that portion of income. But the higher rate applies only to the incremental income above the bracket threshold — not to every dollar earned that year.

How supplemental wage withholding works

This is the source of most commission tax confusion. Per IRS Publication 15 (2026, Section 7), commissions are classified as supplemental wages — a category that includes bonuses, overtime, prizes, and other compensation paid separately from or in addition to regular wages.

For supplemental wages, employers have two withholding methods:

1. Flat rate method (most common)

When commissions are paid on a separate check from regular wages, employers may withhold federal income tax at a flat 22% for commissions up to $1 million in the calendar year. For any commissions that push an employee above $1 million in total commissions and bonuses in a year, the rate on the excess is mandatory 37%.

The 22% rate was established by the Tax Cuts and Jobs Act (TCJA) in 2017 and made permanent law by the One Big Beautiful Bill Act (Pub. L. 119-21) in 2025. IRS Publication 15 (2026) confirms both rates are unchanged.

2. Aggregate method

When commissions are paid together with regular wages on the same check, employers use the aggregate method: they calculate withholding on the combined total using the rep's W-4, apply the resulting rate to the entire payment, and then subtract what would have been withheld on the regular wages alone.

The aggregate method often produces higher single-period withholding than the flat rate, because adding a large commission to a regular paycheck inflates that period's annualized income estimate. The year-end tax liability is identical — only the timing of prepayment changes.

What this means in practice

A rep in the 22% bracket who receives a $20,000 commission check will have $4,400 withheld at the flat rate (22%) — which roughly matches their marginal rate. Withholding and actual tax are close.

A rep in the 32% bracket with the same $20,000 commission will have $4,400 withheld — but their marginal rate on that income is 32%, meaning they owe $6,400. They'll pay the $2,000 difference when they file.

A rep with a $150,000 annual income and effective federal rate of 18% will likely over-withhold at 22% on each commission check and receive a partial refund in spring.

For the detailed breakdown of withholding mechanics across different scenarios, see commission tax rate.

FICA taxes on commission income

Beyond federal income tax, W-2 commission income is subject to FICA withholding — Social Security and Medicare — at the same rates as regular wages.

| FICA tax | Employee share | Employer share |

|---|---|---|

| Social Security | 6.2% | 6.2% |

| Medicare | 1.45% | 1.45% |

| Total FICA | 7.65% | 7.65% |

Social Security wage base (2026): $184,500, per the SSA's 2026 COLA announcement. The 6.2% Social Security withholding applies to the first $184,500 in W-2 wages — once you've crossed that threshold, no additional Social Security tax applies to commissions or salary for the rest of the year.

Medicare: No wage cap. The 1.45% employee share applies to every dollar of W-2 income.

Additional Medicare Tax: Per IRS Topic No. 560, an additional 0.9% applies to wages above $200,000 for single filers ($250,000 for married filing jointly). Employers are required to withhold the extra 0.9% once they pay an employee more than $200,000 in a calendar year. High-earning reps whose commissions push year-to-date wages above $200,000 will see this additional withholding appear on later-year commission checks.

W-2 commission vs. 1099 commission: the real tax difference

For W-2 employees, commissions and salary are treated identically — same income tax brackets, same FICA split with the employer.

For 1099 independent contractors who receive commission payments, the economics are genuinely different. Not because of income tax rates — those are the same — but because of self-employment (SE) tax.

A W-2 employee pays 7.65% in FICA (employee share). Their employer pays another 7.65%. The rep never sees the employer half — it's a payroll cost, not a withholding.

A 1099 contractor has no employer to split FICA with. They pay self-employment tax of 15.3% on net self-employment income — covering both the employee and employer shares:

- 12.4% Social Security (applies to the first $184,500 of net SE income in 2026)

- 2.9% Medicare (no cap)

SE tax is calculated on 92.35% of net SE income, not 100% — this calculation mirrors the deductible employer half. And 1099 contractors can deduct 50% of SE tax paid as an above-the-line adjustment to gross income on Schedule 1 of Form 1040, which reduces the income subject to ordinary income tax.

Even with that deduction, the net effective tax rate on 1099 commission income is higher than the equivalent W-2 income. Most tax advisors recommend 1099 commission contractors set aside 25–30% of gross commission payments to cover combined income tax and SE tax.

Quarterly estimated payments: If you expect to owe $1,000 or more in federal taxes for the year, the IRS requires quarterly estimated payments using Form 1040-ES. Due dates are April 15, June 15, September 15, and January 15. Missing these generates underpayment penalties that accrue regardless of whether you pay the full balance by April.

For a full breakdown of 1099 commission tax treatment, see 1099 commission.

How commissions compare to bonuses for tax purposes

The short answer: they're treated identically.

Both commissions and bonuses are classified as supplemental wages under IRS Publication 15. Both are subject to the 22% flat withholding on separate checks. Both are ordinary income taxed at the same federal brackets at year-end. The IRS draws no tax distinction between a performance bonus and a deal commission.

The practical differences between commissions and bonuses are in structure and timing — commissions are typically formula-driven and tied to closed deals, while bonuses are often discretionary or milestone-based — but neither of these factors changes how they're taxed.

One nuance: if commissions and bonuses are aggregated together and tracked toward the $1 million supplemental wage threshold, a rep receiving both types could reach the 37% mandatory withholding level sooner than if only one type were being counted. In practice, this affects very few W-2 reps, but enterprise reps on high-OTE plans with quarterly bonuses should be aware of it.

For a detailed comparison of how commission and bonus income interact, see commission vs. bonus.

State income tax on commissions

Most states that collect income tax treat commissions as ordinary income and apply a supplemental withholding rate to commissions paid on separate checks.

Common state supplemental withholding rates for 2026:

| State | Supplemental withholding rate |

|---|---|

| California | 6.6% |

| New York | 11.7% |

| Oregon | 8.0% |

| Minnesota | 6.25% |

| Virginia | 5.75% |

| Illinois | 4.95% |

Nine states have no state income tax at all: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Reps in these states don't face state-level withholding on commissions.

For reps who work across state lines or remotely, the rules get more complex. Withholding is typically based on where work is performed — not where the rep lives — which can produce multi-state withholding for reps who split time across locations or work in a different state than their employer. Your state's department of revenue is the authoritative source for state-specific rules.

For more on state-level and federal sales commission tax treatment, see sales commission tax.

Tax planning for sales reps

W-2 employees

The main lever W-2 reps have is their W-4, which controls withholding on salary checks. If you regularly receive large commission payouts, you can adjust your W-4 to withhold additional tax from your salary — effectively pre-paying some of the commission liability through your base pay withholding. IRS Publication 505 (Tax Withholding and Estimated Tax) walks through how to estimate whether your withholding is on track.

Common situations where reps should review their W-4:

- You're in the 32% or 35% bracket and receiving commissions withheld at the 22% flat rate — you likely under-withhold by 10–15 cents per dollar of commission

- You hit a large Q4 commission that pushed your income into a higher bracket than your W-4 anticipated

- You have significant income from a spouse, other sources, or side work that makes the default W-4 calculation too low

Timing commission payouts — pushing a deal's close date to shift income between calendar years — can have tax implications, but constructive receipt rules limit this. If you have the right to receive a commission in 2026 and could collect it, you typically can't defer the tax liability to 2027 simply by waiting to request payment.

The most reliable tax reduction strategy for W-2 reps is maximizing pre-tax retirement contributions. Every dollar contributed to a 401(k) reduces taxable income dollar-for-dollar, up to the 2026 contribution limit of $23,500 (or $31,000 for reps 50 and older with catch-up contributions, per IRS limits for 2026). When commission payouts are finalized, you can use the payroll export to send accurate numbers directly to your payroll provider, reducing the chance of withholding miscalculations.

1099 contractors

For 1099 contractors receiving commissions, the two immediate priorities are:

-

Make quarterly estimated payments. Missing these generates penalties. Use IRS Form 1040-ES to estimate liability. A safe starting point is paying 110% of last year's total tax liability in four equal installments — this meets the safe harbor rule and avoids underpayment penalties regardless of how this year's income turns out.

-

Track business expenses. 1099 contractors can deduct legitimate business expenses — home office, equipment, software, professional services, business travel — against gross commission income. These deductions reduce net SE income, which reduces both income tax and SE tax.

Retirement contributions are also valuable for 1099 contractors. A SEP-IRA allows contributions of up to 25% of net self-employment income (after the SE tax deduction), up to $70,000 for 2026. Solo 401(k) plans offer similar contribution limits with additional flexibility.

What finance teams need to know

When you're designing a commission plan, the quoted commission rate is not the full employer cost. Every dollar of commission paid to a W-2 employee carries an employer-side FICA obligation.

For 2026, the employer pays 7.65% in matching FICA on each commission dollar up to the Social Security wage base ($184,500), and 1.45% Medicare above that threshold. A $10,000 commission payout costs the employer approximately $10,765 in direct payroll costs before overhead or state unemployment taxes.

For reps who've already crossed the $184,500 Social Security wage base, the incremental employer cost is lower — only the 1.45% Medicare match applies. This means a commission plan that pays large Q4 commissions to high earners has a lower employer FICA cost per dollar than the same commissions distributed evenly across the year. If you're exploring how different plan designs affect total employer cost, the commission plan builder lets you model tiered and accelerator structures before committing.

For accounting treatment of commission expense under ASC 606 — where sales commissions paid to acquire customer contracts must be capitalized and amortized rather than expensed immediately — see commission accounting and ASC 606 commission.

Tools like Carvd calculate commissions at the deal level, giving payroll accurate per-rep payout numbers and giving finance a clean record for both payroll processing and expense accounting.

Quick reference: commission tax rates for 2026

| Item | Rate / Value | Source |

|---|---|---|

| Federal supplemental withholding (under $1M/year) | 22% flat | IRS Pub. 15 (2026), Section 7 |

| Federal supplemental withholding (over $1M/year) | 37% mandatory | IRS Pub. 15 (2026), Section 7 |

| Social Security withholding (W-2, employee) | 6.2% up to $184,500 | SSA 2026 COLA announcement |

| Medicare withholding (W-2, employee) | 1.45% (no cap) | IRS FICA guidance |

| Additional Medicare Tax | 0.9% above $200K single | IRS Topic No. 560 |

| Self-employment tax (1099) | 15.3% on 92.35% of net SE income | IRS Topic No. 554 |

| Employer FICA match | 7.65% up to $184,500 | IRS Pub. 15 (2026) |

| Commissions taxed higher than salary? | No — same ordinary income brackets | IRS IRC §61 |

Related guides in this series

- Commission tax rate — withholding rates, FICA breakdown, and what your commission check actually shows

- Is commission taxed differently? — why commission checks look taxed more and what's actually happening

- 1099 commission — self-employment tax, quarterly estimated payments, and contractor-specific treatment

- Commission vs. bonus — how the two compare in structure, tax treatment, and comp plan design

- Sales commission tax — sales-specific considerations for commission income

- Commission accounting — ASC 606 treatment and expense recognition for finance teams

Last updated: March 22, 2026