Is Commission Taxed Differently Than Salary? The Honest Answer

Commission is ordinary income — same tax brackets as salary. But withholding works differently, which is why your commission check looks taxed more. Here's what's actually happening.

Commission income is not taxed differently than salary — not for federal income tax purposes. The IRS classifies commissions as ordinary income, subject to the same brackets as your base pay. A dollar earned in commission generates the same tax liability as a dollar earned in salary.

The confusion is real, though, and it comes from how commissions are withheld, not how they're taxed. If your commission check looks like it's getting hit harder than your salary, you're looking at a payroll calculation method, not a higher tax rate.

Why commissions and salary are taxed the same

Under the Internal Revenue Code, "ordinary income" covers most earned income — wages, salary, bonuses, tips, and commissions. All of it flows into the same federal tax brackets. In 2026, those brackets range from 10% to 37%, and your bracket is determined by your total annual income, not by where the money came from.

Your W-2 at year-end doesn't show "salary income" and "commission income" in separate boxes with different rates. It shows total wages (Box 1). The IRS applies your brackets to the total.

For most sales reps, this means the same dollar can shift between salary and commission without changing the year-end tax outcome. A rep with $80,000 in base salary and $40,000 in commissions has the same tax liability as a rep with $120,000 in salary and no commissions — assuming identical deductions and filing status.

How withholding works differently

Here's where the confusion comes from: while tax liability is the same, withholding is not.

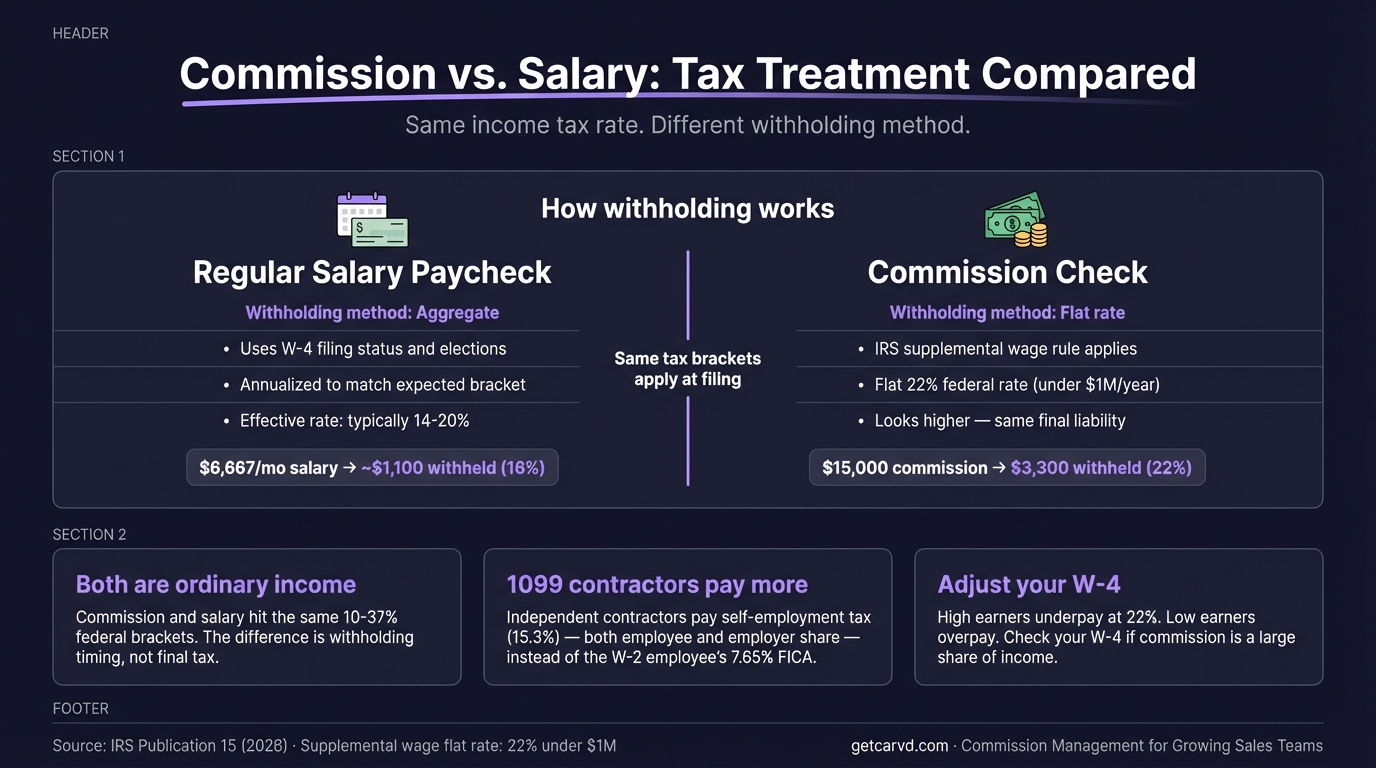

When an employer pays commissions separately from regular wages, the IRS classifies commissions as supplemental wages. For supplemental wages, employers have two withholding options per IRS Publication 15:

- Flat rate method — withhold 22% flat, regardless of the rep's income or W-4 settings

- Aggregate method — add the commission to the most recent regular paycheck and calculate withholding on the combined total using the W-4

Most employers use the flat 22% method because it's simpler. The aggregate method produces higher single-period withholding for most reps (because stacking commission on top of salary inflates that payroll period's annualized income estimate), even though it produces the same year-end outcome.

What this means: A $25,000 commission check will have $5,500 withheld for federal income tax at the flat rate. Your salary paycheck for the same period might show $600 in federal withholding on $5,000 in wages — a 12% effective in-period rate. Same marginal tax rate, dramatically different withholding pattern.

The IRS reconciles this at year-end. If 22% over-withheld compared to your actual liability, you get a refund. If 22% under-withheld (which happens for reps in the 32% or 35% bracket), you owe the difference when you file.

When commission IS taxed differently: the 1099 situation

For W-2 employees, the "same as salary" answer holds. For 1099 contractors, it's different — and the difference is real.

A 1099 contractor receives commission gross, with no withholding. At tax time, they owe:

- Federal income tax — same ordinary income brackets as a W-2 employee

- Self-employment (SE) tax of 15.3% — covering both the employee and employer shares of Social Security and Medicare FICA taxes

W-2 employees only pay the employee share of FICA: 6.2% Social Security (up to the $184,500 wage base in 2026) and 1.45% Medicare. Their employer matches those contributions. 1099 contractors pay both shares themselves — 12.4% Social Security and 2.9% Medicare — because there's no employer to pick up the other half.

The one offset: 1099 contractors can deduct half their SE tax from gross income on Schedule 1, which reduces the total sting somewhat. But the net result is still that independent contractor commission income carries a heavier FICA burden than equivalent W-2 income. If you're trying to compare net take-home across structures, the commission calculator can model payout amounts for different plan types.

Most tax advisors recommend 1099 commission contractors set aside 25–30% of gross commission payments to cover combined income tax and SE tax. The right percentage depends on your total income and deductions, but 25% is a reasonable floor for most.

For more on 1099-specific commission tax treatment, see 1099 commission.

The aggregate method and why it can look worse

If your employer uses the aggregate method instead of the flat 22%, your commission period withholding may look even higher than the flat rate — which compounds the perception that commissions are being penalized.

Here's why: the aggregate method takes your commission plus your most recent regular paycheck and treats the combined total as representative of your annual income. If your regular semi-monthly paycheck is $4,000 and your commission is $20,000, the payroll system annualizes $24,000 for that period — projecting $576,000 in annual income — and withholds at that bracket.

The result on that single paycheck can look shockingly high. But it's still just withholding. The year-end tax liability is the same. Any over-withheld amount is refunded when you file. If you want to track exactly how much was withheld versus what you actually earned per deal, a commission spreadsheet template can help organize those numbers before tax season.

State taxes: a genuine wrinkle

Federal tax is clear: commission and salary are treated identically. State tax is messier.

Most states follow the federal classification and treat commissions as ordinary income. But supplemental withholding rates vary significantly by state. In 2026, California applies a 6.6% supplemental withholding rate to commissions paid on separate checks. New York applies 11.7%. These are withholding rates, not final tax rates, but they stack on top of federal withholding and amplify the perception of higher taxation.

Nine states have no state income tax at all — Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming — so reps there don't face this issue at the state level.

For reps who work across state lines or remotely, the rules get more complicated. Withholding is typically based on where work is performed, not where the rep lives. The authoritative guidance is IRS Publication 15-A and your state's department of revenue.

Practical implications

For W-2 reps: Commission income is not taxed at a higher rate than salary. What changes is the timing and method of withholding. If you're regularly getting large commission payouts and concerned about over- or under-withholding, you can adjust your W-4 to increase withholding on your salary checks. IRS Publication 505 walks through the estimation process.

A common scenario for high performers: they're in the 32% or 35% bracket, but their commissions are withheld at 22%. They owe more at filing. The fix is either increasing salary withholding via W-4 adjustment or making estimated payments during the year.

For 1099 contractors: Commission income is genuinely taxed differently. Not at a higher income tax rate, but with the additional SE tax layer. Factor that into how you price your work and set aside from each commission payment.

For finance teams: When calculating the true employer cost of a commission plan, add 7.65% in matching FICA on each commission dollar (up to the Social Security wage base). A $15,000 commission payout costs roughly $16,148 in direct payroll costs before overhead. Tools like Carvd calculate payouts at the deal level, giving payroll accurate numbers and giving finance a clean record for cost accounting. Once payouts are finalized, the payroll export sends the exact amounts to your payroll provider so withholding is applied to the correct figures.

For a full breakdown of withholding rates and how they interact with different tax brackets, see commission tax rate. For the broader overview of how commissions move through federal taxes, see how are commissions taxed.

The short answer

Commission is ordinary income. It's taxed at the same federal brackets as salary. The difference is withholding — a payroll mechanics issue, not a tax policy one. The exception is 1099 contractor commission, which carries a real SE tax premium that W-2 employees don't face.

The clearest sign that it's a withholding issue rather than a tax issue: reps who hit large commission quarters often get the "extra" withheld returned as a refund in April. If commissions were genuinely taxed higher, there would be no refund — just a larger bill.

Last updated: March 22, 2026