1099 Commission: Contractor Comp Plans Explained

1099 commission contractors receive gross pay with no withholding and owe 15.3% self-employment tax. Here's how contractor comp plans work and what companies need to know.

When a company pays commission to an independent contractor rather than an employee, the mechanics of how that money moves — and how it's taxed — are fundamentally different from a W-2 arrangement. The contractor receives the full gross amount, no withholding, and owes both income tax and self-employment tax come April.

Most sales teams use W-2 employees for their core reps. But 1099 commission arrangements are common for outside agents, referral partners, manufacturers' representatives, and specialist contractors brought in on a deal basis. If you're designing or receiving this kind of comp plan, the tax and structural differences matter.

For the broader picture of how commissions are taxed, see how are commissions taxed.

What makes a commission arrangement "1099"

The term "1099 commission" refers to commission paid to an independent contractor, reported on Form 1099-NEC (Non-Employee Compensation). It's not a legal status you choose — it's a classification that the IRS determines based on the actual working relationship.

The IRS uses three categories of evidence to assess whether someone is an employee or an independent contractor:

Behavioral control. Does the company dictate how, when, and where work is performed? Employees follow detailed work instructions. Contractors control their own methods.

Financial control. Does the contractor invest in their own equipment, work for multiple clients, and absorb their own business expenses? Contractors typically have profit-and-loss exposure. Employees don't.

Nature of the relationship. Is the work integral to the company's core business? Is there an indefinite engagement, or a project-based one? Is there a written contract specifying the independent nature of the relationship?

No single factor is determinative — the IRS looks at the full picture. But the pattern that creates risk is when someone is treated in practice like an employee (fixed hours, direct supervision, exclusive relationship) while being paid as a contractor.

Some states apply a stricter test. California, Massachusetts, and New Jersey use the ABC test, which presumes workers are employees unless the company can prove all three: the worker is free from the company's direction, the work is outside the company's usual course of business, and the worker has an independently established trade or occupation. The ABC test makes contractor classification significantly harder in those states.

How 1099 commission comp plans are structured

Independent contractor comp plans share the basic mechanics of W-2 commission structures — flat rate, tiered, per-product — but there are practical differences in how they're designed.

Straight commission is most common. Most 1099 contractor arrangements are pure commission with no base. The contractor earns a percentage of the deals they close. Without the overhead of a base salary, the commission rate is often higher than what a W-2 rep would receive.

Typical 1099 commission rates for sales roles run 5–20% of deal value depending on the industry, sales cycle length, and the amount of support the company provides. Real estate agents, insurance brokers, and manufacturers' reps often operate in this range. The rate has to price in what the contractor doesn't get: no benefits, no base, no employer FICA match, no expense reimbursement.

Payment triggers and timing matter more. With W-2 reps, commissions often run through payroll and pay out on a fixed schedule. With 1099 contractors, the payment terms need to be explicit in the contract: when does a deal count as closed, when does the commission pay (on invoice, on payment, on contract), and what happens to commission if the deal cancels or the customer doesn't pay.

Clawback provisions require care. Commission clawbacks are standard in W-2 arrangements. With 1099 contractors, clawback provisions are enforceable but need to be clearly written into the contractor agreement. An ambiguous clawback clause on a 1099 arrangement is a dispute waiting to happen — particularly for long sales cycles where the contractor may have moved on by the time a deal falls through.

For the mechanics of clawback design, see commission clawbacks.

Tax implications for the contractor

This is where 1099 commission differs most from W-2 commission.

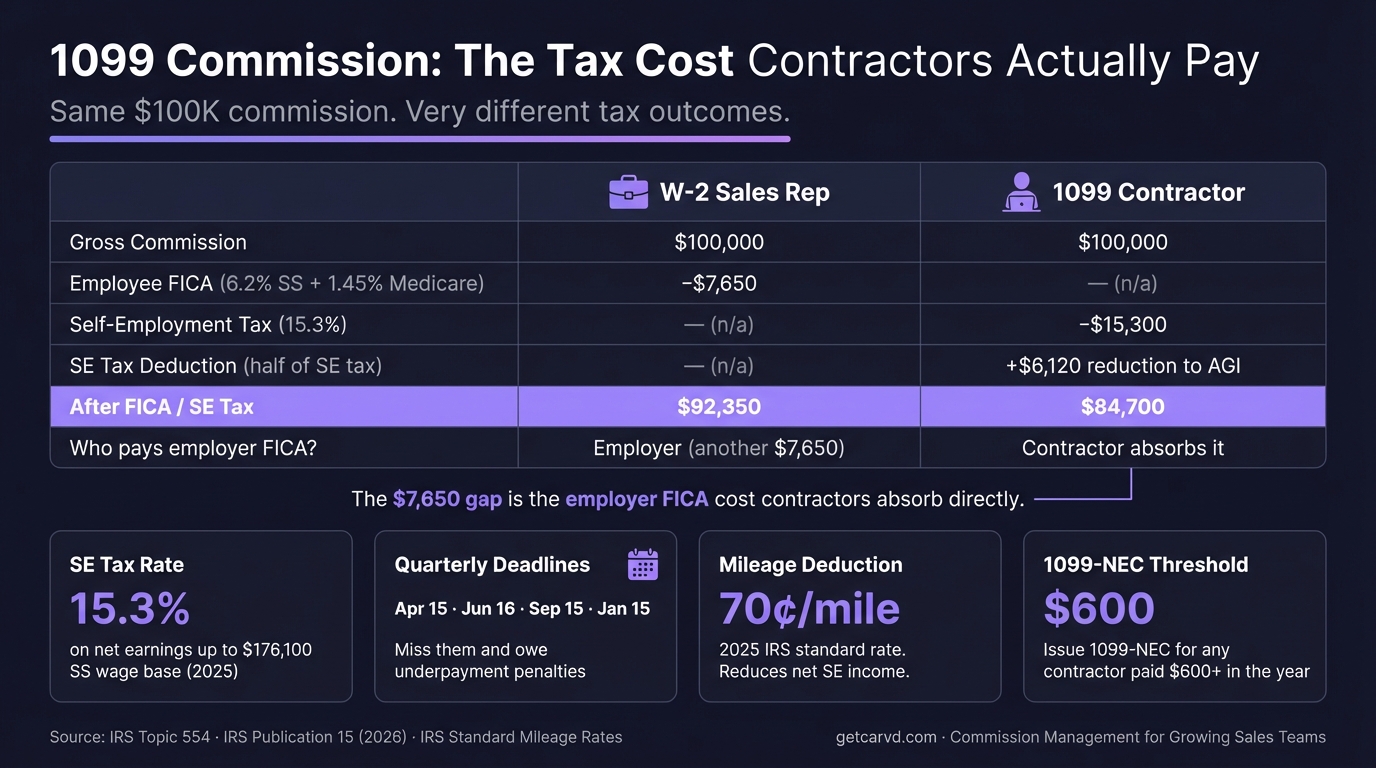

A W-2 sales rep receives a commission check with federal income tax withheld at the 22% supplemental rate, plus FICA withholding (6.2% Social Security + 1.45% Medicare, on the employee's side). The employer matches the FICA portion. The rep never sees the employer's 7.65%.

A 1099 contractor receives the gross commission amount with no withholding at all. At tax time, they owe:

Federal income tax. Same brackets as a W-2 employee — 10% to 37% on ordinary income. No special rate for contractors.

Self-employment (SE) tax. This is the material difference. SE tax is 15.3% on net self-employment income — 12.4% Social Security and 2.9% Medicare. This covers both the employee and employer sides of FICA, because there's no employer to pay the other half.

The Social Security portion applies only to the first $184,500 of net self-employment income in 2026 (per the Social Security Administration). Medicare has no cap. For high-earning contractors, there's also an Additional Medicare Tax of 0.9% on SE income above $200,000 (single) or $250,000 (married filing jointly).

One offset: 1099 contractors can deduct half their SE tax from gross income on Schedule 1 of Form 1040 — replicating the employer-paid share that W-2 employees receive without seeing. This reduces the effective SE tax burden somewhat, but the net still exceeds what a W-2 employee pays. Tracking gross payouts deal-by-deal in a commission spreadsheet template makes it easier to calculate quarterly SE tax obligations accurately.

Most tax advisors suggest 1099 commission contractors set aside 25–30% of gross commission income to cover both federal income tax and SE tax. The right number depends on total income and deductions, but 25% is a reasonable floor.

Quarterly estimated payments

1099 commission contractors with no employer withholding are responsible for paying taxes as they earn. If you expect to owe $1,000 or more in federal taxes for the year, the IRS requires quarterly estimated payments using Form 1040-ES.

The 2026 due dates:

| Quarter | Period covered | Due date |

|---|---|---|

| Q1 | Jan 1 – Mar 31 | April 15, 2026 |

| Q2 | Apr 1 – May 31 | June 15, 2026 |

| Q3 | Jun 1 – Aug 31 | September 15, 2026 |

| Q4 | Sep 1 – Dec 31 | January 15, 2027 |

Missing estimated payments triggers an underpayment penalty. The penalty is calculated on the underpaid amount for each quarter — it's not a one-time fine, it accrues. The penalty applies even if you pay the full balance by April 15.

Contractors with highly variable commission income (large deal-based payouts in some quarters, nothing in others) need to model their estimated payments carefully. Paying in equal quarterly installments works if your income is roughly even across the year. If most of your commission hits in Q4, front-loading payments in Q1–Q3 can over-pay, but it avoids penalty exposure. Running your pipeline through the commission calculator each quarter gives you a forecast of variable income to base your estimated payments on.

The 1099-NEC form

Companies that pay commission to contractors are required to file Form 1099-NEC and provide a copy to the recipient.

As of 2026, the reporting threshold is $2,000 per contractor per calendar year — raised from the previous $600 threshold under the One Big Beautiful Bill Act, signed July 4, 2025, per IRS guidance. The threshold will be adjusted for inflation annually starting in 2027.

The 1099-NEC must be sent to contractors by January 31 of the following year. The same deadline applies to filing with the IRS.

One important clarification: the $2,000 threshold applies to the reporting obligation, not the tax obligation. Contractor commission income below $2,000 is still taxable. The contractor is still required to report it on their return, even if no 1099 is issued.

1099-NEC covers service-based non-employee compensation — what most sales commission arrangements fall under. It's distinct from 1099-MISC, which covers other miscellaneous income like rent, royalties, and prize winnings that aren't compensation for services.

What companies need to know

Misclassification risk is real. If a rep is functioning like an employee but classified as a 1099 contractor, the IRS can reclassify the relationship and assess back taxes, interest, and penalties on both the company and the individual. The employer becomes liable for both sides of FICA on the reclassified income. Some state labor agencies add additional claims for back wages and benefits.

Before classifying a sales role as 1099, verify that the relationship actually fits. Contract-based, project-driven, multi-client arrangements typically qualify. Exclusive, supervised, indefinite-term arrangements typically don't.

Contractor comp plans need explicit terms. Because there's no payroll infrastructure governing the payment, the contractor agreement has to spell out: commission rate, deal eligibility criteria, payment timing, clawback provisions, and what happens to in-flight deals if the arrangement ends. Ambiguity in any of these creates disputes that are harder to resolve than W-2 comp disputes because there's no internal payroll process as a reference point. The commission plan builder helps formalize these terms into a structured plan before the first deal closes.

Commission tracking applies equally. Whether reps are W-2 or 1099, companies need accurate deal-level commission records. Contractors have the same interest in seeing how their payouts were calculated as W-2 employees do — arguably more, since they're running their own P&L and need accurate numbers for their own quarterly tax planning.

Tools like Carvd calculate commissions at the deal level with a full breakdown of how each payout was derived. For companies managing a mix of W-2 and 1099 sales roles, having a single system that produces auditable commission records simplifies both internal payroll and the documentation you'll need when contractors reconcile their 1099-NECs.

1099 vs W-2 commission: the tax comparison

| W-2 employee | 1099 contractor | |

|---|---|---|

| Withholding | Employer withholds income tax + FICA | No withholding — contractor pays directly |

| FICA | Employee pays 7.65%; employer matches 7.65% | Contractor pays full 15.3% SE tax |

| SS wage base (2026) | $184,500 | $184,500 |

| Quarterly estimated payments | Not required (withholding covers it) | Required if $1,000+ owed |

| 1099-NEC issued? | No — W-2 issued instead | Yes, if $2,000+ paid in year |

| Deductible expenses? | Limited (mostly unreimbursed W-2 expenses aren't deductible post-TCJA) | Yes — Schedule C deductions available |

For more on commission tax for W-2 reps, see commission tax rate and is commission taxed differently. For the employer-side accounting treatment of commission expense, see commission accounting.

Last updated: March 22, 2026