Incentive Pay: Types, Tax Implications, and Structures

Incentive pay is variable compensation tied to performance — commissions, bonuses, profit sharing, or equity. Here's how each type works and how it's taxed.

Incentive pay is variable compensation earned by hitting a defined target — closing deals, reaching quota, exceeding a profit threshold, or achieving a specific objective. It's the portion of total compensation that changes based on results, as opposed to the fixed salary that arrives regardless.

For sales roles, incentive pay is the core of how compensation works: commissions that scale with performance, accelerators for overperformance, and SPIFFs for specific behaviors. For non-sales roles — managers, executives, and sometimes individual contributors — it shows up as performance bonuses, profit sharing, or equity.

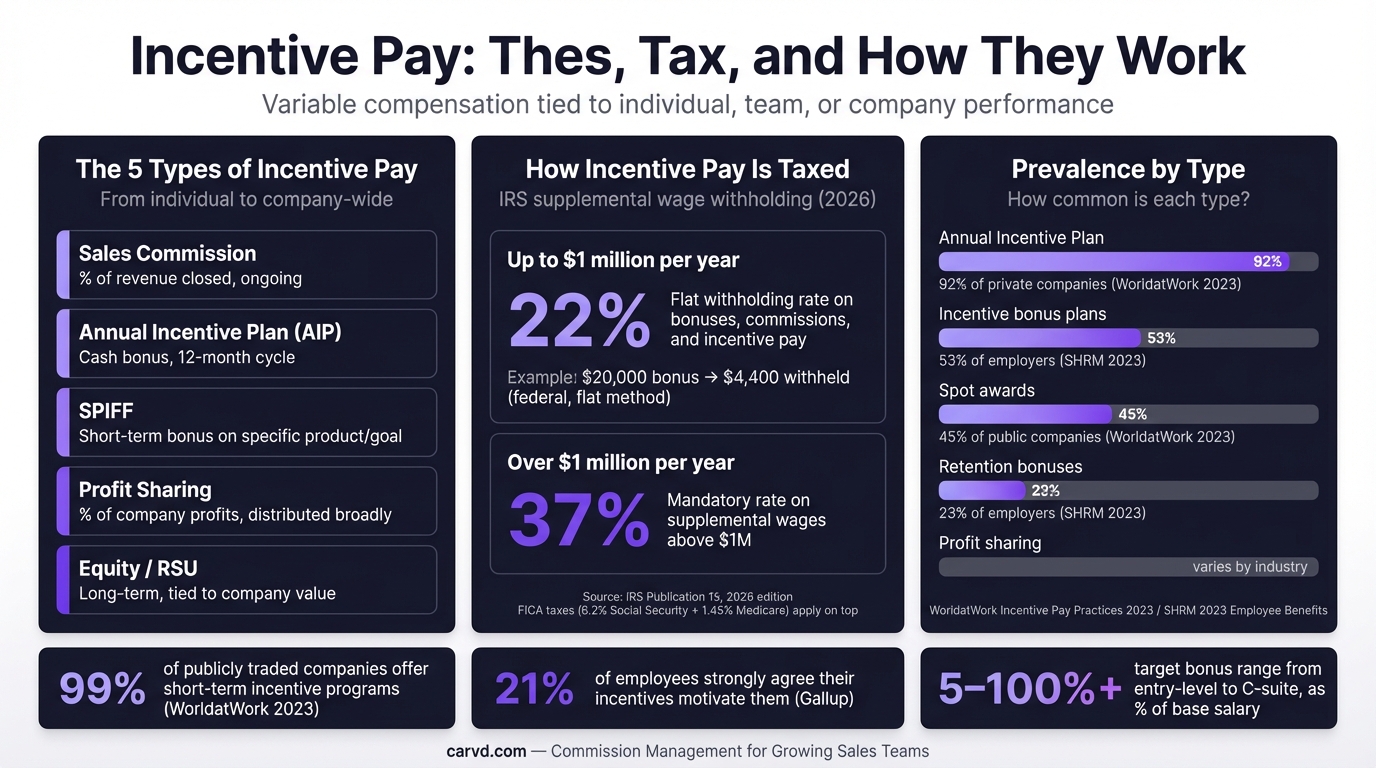

According to WorldatWork's 2023 Incentive Pay Practices Survey of 706 organizations, 92% of privately held companies and 99% of publicly traded companies run short-term incentive programs. That near-universal adoption reflects how central incentive pay has become to compensation design across functions.

Types of incentive pay

Commissions

Commission is the most common form of incentive pay for sales roles. A rep earns a percentage of revenue, ACV, or deal value for each closed deal. Commission is ongoing and directly tied to individual output — a rep knows their rate and can calculate expected earnings as deals close.

For a full breakdown of commission structures — flat, tiered, per-product, and draw against — see the sales commission structure guide.

Performance bonuses

Bonuses are one-time payments triggered by hitting a predefined target: annual quota attainment, a revenue milestone, or a management objective. They're evaluated and paid after the measurement period closes, which distinguishes them from commissions that are calculated deal-by-deal in real time.

Annual incentive plans (AIP) are the most common bonus structure for managers and executives. For detail on how they're designed, see the annual incentive plan guide.

Profit sharing

Profit sharing distributes a portion of company earnings to employees, typically on a quarterly or annual basis. The payout pool is defined as a percentage of pre-tax profit, then divided among eligible employees.

Profit sharing is common in manufacturing, professional services, and mature tech companies. It aligns employee behavior with overall company profitability rather than individual performance metrics — which is its strength and limitation. A rep who closes great deals can't directly control whether the company hits its profit target.

Stock options and equity

Equity-based incentive pay — stock options, RSUs, or performance shares — is a long-term incentive that vests over a defined schedule, typically 3–4 years with a one-year cliff. It's prevalent at startups and public companies, and it aligns employee interests with shareholder value over time.

For sales teams, equity is usually secondary to cash commissions. For executives and early employees at growth-stage companies, it's often the larger part of total compensation.

SPIFFs

A SPIFF (Sales Performance Incentive Fund) is a short-term cash bonus for completing a specific, defined action — closing a particular product line, booking demos in a new vertical, or hitting a target within a compressed window. SPIFFs are layered on top of regular commissions, not substituted for them.

For a detailed guide on when SPIFFs work and how to design them, see what is a SPIFF in sales.

Gainsharing

Gainsharing is a team-based incentive where employees share in productivity improvements or cost savings. It's most common in manufacturing and operations, where measurable efficiency gains can be directly tied to payouts. For sales organizations, it appears occasionally in customer success or operations teams where individual deal attribution isn't the right metric.

How incentive pay is taxed

The IRS classifies commissions, bonuses, and most other forms of variable pay as supplemental wages — a distinct category from regular wages under federal tax law (IRS Publication 15, Circular E).

The flat supplemental wage withholding rate is 22% for payments up to $1 million per year. For supplemental wages exceeding $1 million in a calendar year, the mandatory withholding rate rises to 37%.

Two things worth understanding about this rate:

It's a withholding rate, not a final tax. When an employer pays a commission or bonus separately from regular wages, 22% is withheld upfront. Employees reconcile actual tax liability at filing. Someone in the 32% marginal bracket will owe more; someone in the 12% bracket may get a refund.

Employers have a second option. Instead of the 22% flat rate, an employer can aggregate supplemental wages with regular wages in the same paycheck and withhold at the employee's standard W-4 rate. Both methods are compliant with IRS rules.

Commissions and bonuses are treated identically — both are supplemental wages. There is no special "commission tax rate" separate from the bonus tax rate. When large commission checks feel heavily taxed, that's the 22% withholding rate at work, not a permanently higher tax burden.

Pay mix: how much of compensation should be incentive pay

Pay mix is the ratio of base salary to variable pay at 100% quota attainment. For sales roles, it's the most consequential structural decision in comp plan design.

Bridge Group's 2024 SaaS AE Benchmark Report (covering 170+ B2B SaaS companies) puts the median AE pay mix at 53% base / 47% variable. Nearly half of expected annual earnings come from hitting quota.

Use the OTE calculator to model how different pay mixes translate to expected earnings at various attainment levels. Standard benchmarks by role:

| Role | Typical pay mix (base / variable) |

|---|---|

| Direct quota-carrying AE | 50–60% base / 40–50% variable |

| SDR | 65–70% base / 30–35% variable |

| Account Manager | 60% base / 40% variable |

| Sales Manager | 65% base / 35% variable |

| Non-sales manager | 80–85% base / 15–20% variable |

Higher variable share is appropriate for roles with direct, measurable revenue impact. Lower variable fits roles where contribution to revenue is indirect or where the sales cycle is long enough that quarter-to-quarter swings in pay would create retention problems.

Alexander Group's 2024 Sales Compensation Trends Survey found that 66% of organizations are actively increasing their pay-for-performance levers — shifting more compensation from fixed to variable. The primary drivers cited: margin pressure and the need to tie comp expense more directly to revenue outcomes.

Short-term vs long-term incentive pay

Incentive pay is typically split into two categories:

Short-term incentives (STI) pay out within the current performance year. Commissions, quarterly bonuses, annual incentive plans, and SPIFFs all fall here. For most sales teams, STI is the primary tool for shaping daily behavior.

Long-term incentives (LTI) vest over multiple years. Stock options, RSUs, and performance shares are the most common forms. LTI is standard at public companies and common at late-stage startups — primarily used to retain and align employees with company growth over a longer horizon.

For sales teams with 5–50 reps, the relevant layer is almost always STI. LTI becomes relevant when designing comp for sales leaders and executives, or when an early-stage company is using equity to offset below-market cash salaries.

The sales incentive plan guide covers how STI components — base commission, accelerators, and SPIFFs — fit together into a complete plan structure.

What makes incentive pay actually work

Research on incentive design points to a few consistent drivers:

Line of sight. Reps who can calculate their incentive pay within two minutes of closing a deal outperform those who earn more but can't trace the connection. Complexity kills the behavioral signal. A plan with five metrics and an annual multiplier based on renewal rates calculated the following quarter is one where reps stop tracking their own progress.

Fewer metrics, higher weight. Spreading variable pay across five metrics dilutes each one. If customer satisfaction is worth 5% of variable comp, reps will ignore it. At 20% weight, they'll manage it. Most research on incentive design supports one or two primary metrics per role. The comp plan builder lets you configure these metrics and see how different weightings affect payouts before you commit.

Payout speed. The closer the reward is to the action, the stronger the motivational connection. Monthly commissions are standard; anything beyond 45 days starts to break the feedback loop that incentive pay is designed to create. Fast payroll export capabilities help close the gap between deal close and payment.

Transparency. Reps who can see exactly how their incentive pay was calculated — deal by deal — are less likely to maintain personal shadow accounting spreadsheets to verify their own payouts. That shadow accounting is a hidden tax on selling time, and it's a signal that reps don't trust the numbers they receive. Tools like Carvd show reps a full breakdown of how each deal contributed to their payout, alongside the commission statement that goes to payroll.

For a deeper look at how incentive compensation fits into the broader management system — including how ICM software supports automated, transparent incentive administration — see the incentive compensation management guide.

Last updated: March 22, 2026